New rates have led to more gifts

As of 1 July 2015 the tax rates for gifts of immovable property were reformed and reduced. Two aspects were subject to the reform: the categories for the recipients were simplified and the tax rates were cut. The scheme was later adopted by the Brussels Capital-Region and the Walloon Region, which introduced a number of (more limited) amendments.

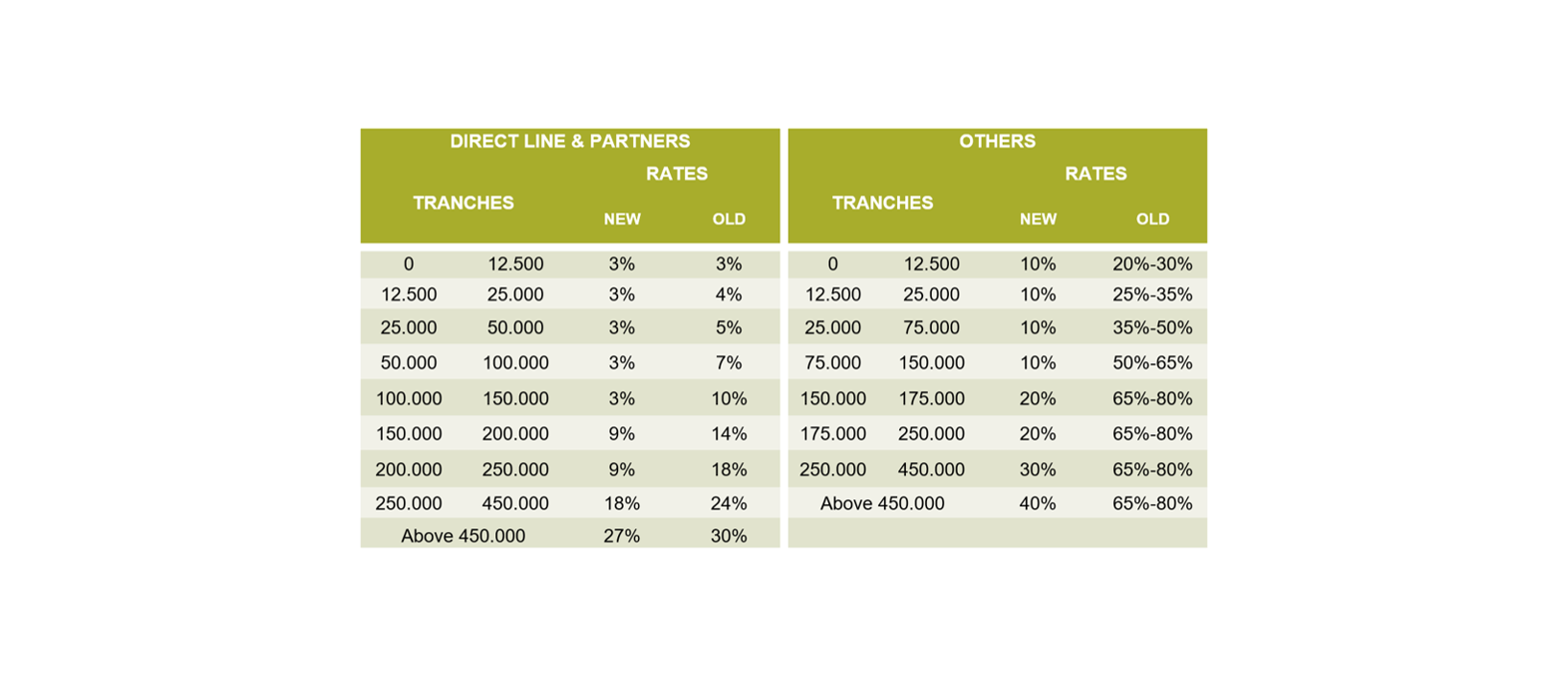

The tables below provide an overview of the new rates for gift tax:

For a residence worth €150,000 the rate is still 3%, while previously it could have amounted 10% (for direct line rates). If the residence was gifted to family members not in the ‘direct line’ the rate today will be 10%, while previously it could reach 65%.

An example further illustrates the changes:

- A married couple, married under a regime of community of property comprising only of property acquired after their marriage, own an investment property that is worth €800,000 and wish to give it to their 2 children.

Under the former scheme, the gift tax would amount to €70,500, with each of the children consequently having to pay €35,250.

If the parents did not give them the property, and the children simply inherited it, total inheritance tax of €60,000 would be payable (if the parents died simultaneously), with each of the children having to pay €30,000.So simply leaving things be and letting the apartment be inherited in due course was around €10,000 more advantageous than gifting it. And so it made sense that very few people decided to give immovable property away.

Under the new scheme, however, the total gift tax is down to €36,000, making gifts a lot more appealing.

The cut to the rates has now led to a considerable increase in the number of immovable properties that are gifted. Until the close of last October over 15,300 instruments of gift were executed, for a total sum of 2.3 billion euros (source: Notaris.be), and a great many more gifts are expected to follow before the end of the year.

Flemish Minister of Finance and Budget Bart Tommelein has voiced his satisfaction, calling it a ‘win-win-win situation’, as it benefits citizens, the economy and the Flemish government. Now that immovable assets are more frequently transferred while the owner is still alive, the revenues are also received by the Flemish authorities more quickly.

The cut to the rates has led to new opportunities for planning your assets, and making gifts of immovable property is certainly worth considering. However, it remains an exercise where every case must be examined individually as, outside of the financial and tax aspects, there are numerous other factors that must be weighed up. Just a few examples:

- what is the true individual situation?

- what are your future expectations?

- how many buildings do you own, what are they worth and will you purchase more?

- what type of immovable property is involved?

- what is the age of the grantor and the recipient?

These are all questions that should first be discussed in a personal consultation before deciding on whether or not immovable property should be gifted.

What does the future hold?

Aside from the reduction of the gift tax, steps have also been taken to update our inheritance law, and there have been proposals to cut the high inheritance taxation, especially rates for collateral relatives and between non-relatives.

For further information, you can always contact our Estate Planning team.

Contact one of our experts