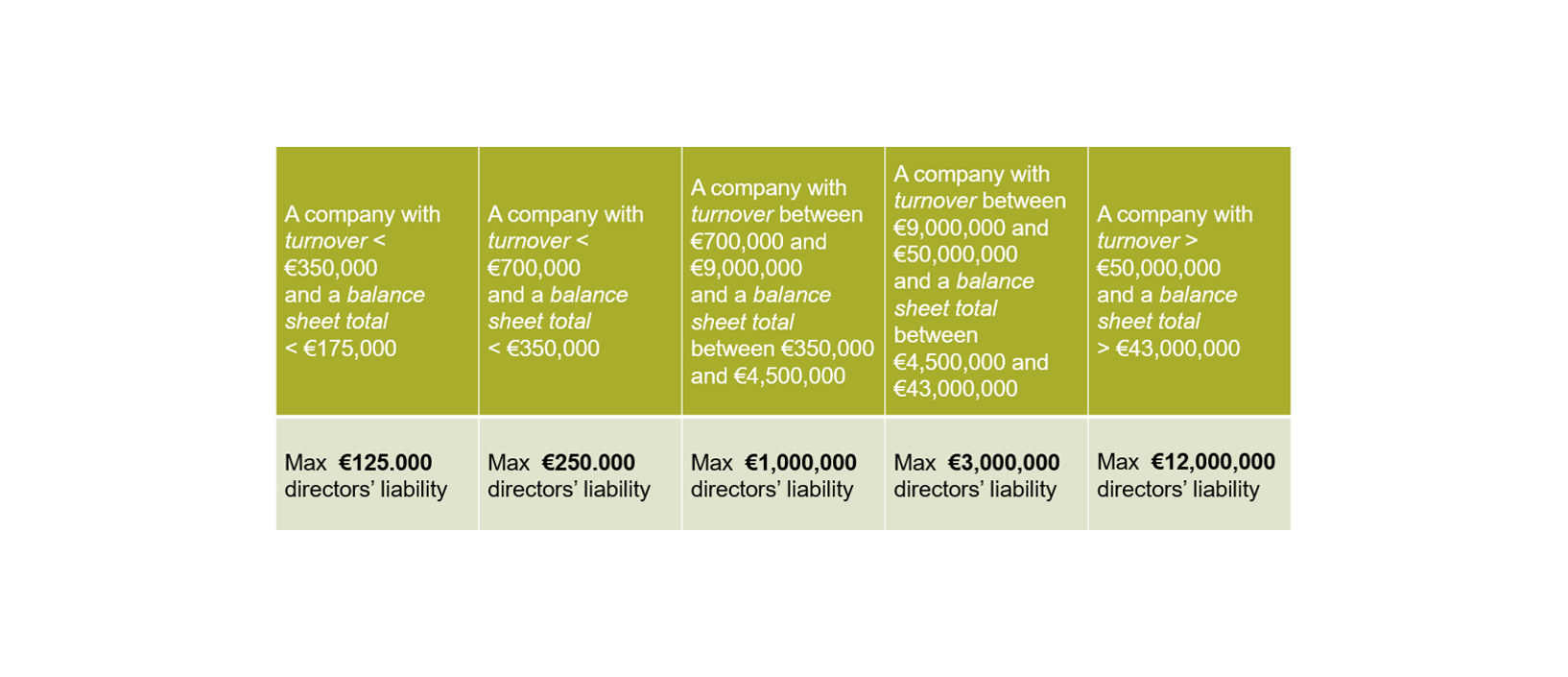

From the entry into force of the CAC, maximum limits on the liability of directors will apply. These limits have been made dependent on the average turnover (excluding VAT) and the average balance sheet total of the last three financial years. The maximum compensation amounts are linked to the economic size of the company or association. That way, they are a clear yardstick of the social impact of the company.

The legislator justified the introduction of this limitation of liability by highlighting the better predictability and insurability of directors' risks. The limitation of liability might also be an incentive to attract international companies, by aligning it with directors' liability in our neighbouring countries. Finally, the aim is to eliminate the unjustified discrepancy between the liability of directors and the liability of top managers who do not hold a directorship.

The limitation of liability of the management body will apply both internally and vis-à-vis third parties. It can also be invoked on a fact-by-fact basis, irrespective of the number of claimants or the different qualifications to which a fact or range of facts gives rise. It goes without saying that the limitation of liability only applies to actions taken by the director in their capacity as director.

For the smallest companies and non-profit organisations, the liability is limited to €125,000. In contrast, liability is limited up to €12 million for the largest companies and non-profit organisations. The limitation of liability is applicable both vis-à-vis legal entities and third parties, regardless of the basis of the claim. Below you will find a brief overview.

It is not possible to envisage a contractual limitation of liability within these legal thresholds. Nor can any agreements be made to indemnify the legal entity or any subsidiaries against any liability. Discharge may still be granted to a director. In principle, this excludes any liability claim. It is also interesting to highlight the fact that legal entities can take out liability insurance for their directors.

However, thanks to a last-minute amendment, this limitation of liability needs to be qualified to a significant extent. That is because it is not possible to invoke the limitation of liability in the event of:

- A minor error that is more habitual than accidental.

- A serious error or fraudulent intent, or intent to cause damage on the part of the person held liable.

- A manifestly gross error, or in cases of wrongful trading.

- Joint and several liability regarding fiscal debts such as VAT and the withholding tax on wages.

- Directors are subject to guarantee obligations (e.g. if the director is legally responsible for an undertaking made by someone else).

As a result, the limitation of directors' liability will only apply to accidental minor errors. Such errors rarely resulted in directors' liability in the past.

The introduction of a limitation of directors' liability therefore seems to have missed the mark in some respects. As such, the necessary caution still needs to be exercised by anyone fulfilling a director's mandate.

The limitation on directors' liability will apply to facts giving rise to damage occurring after 1 January 2020, which is the date on which the CAC will in principle apply to existing legal entities. A legal entity may also opt to apply the new provisions earlier. In such cases, the limitation of liability will apply in advance. Directors of new companies and companies which opt to apply the CAC earlier can enjoy the limitation of liability from 1 May 2019 at the earliest.

Contact one of our experts