Fact #1: there is a lot of cash in the markets.

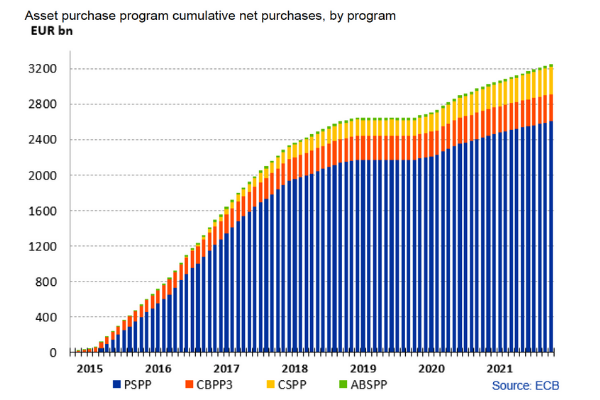

Since 2015 and up to the end of 2021 the European Central Bank (ECB) has pumped a staggering amount of money into the markets: 3200 billion euro to be precise.

This policy started as a response to the financial crisis of 2008 when interbank trading came to a virtual end, whereby the ECB provided additional liquidity to banks with immediate liquidity needs. Due to the covid crisis, those measures to give oxygen to the economy in order to prevent a collapse, were never really scaled back.

The same happened in other developed countries, most importantly in the United States where the FED has initiated Quantitative Easing programs three times in recent years: 2010, 2012, and in 2020 in response to the COVID-19 pandemic.

Fact #2: that money finds its way to private equity.

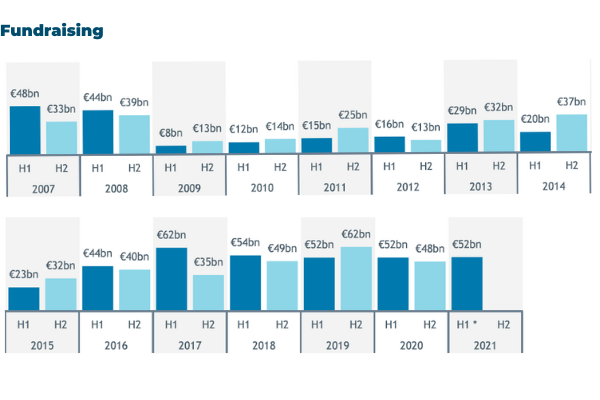

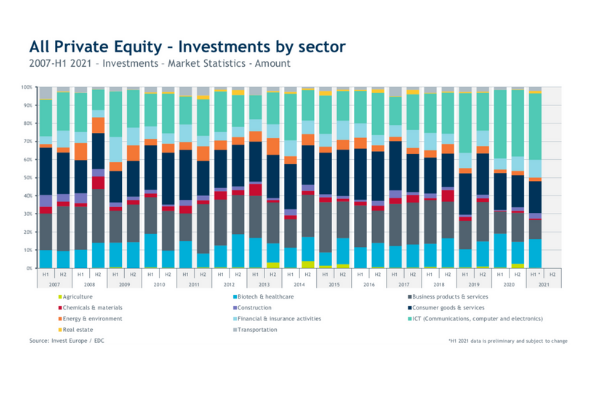

The sharp increase in available cash is reflected in the fundraising and investments by private equity (PE).

Fundraising figures gathered by Invest Europe show that the total value remains at continuous high levels during the last five years. In the first half of 2021, 52 billion euro was raised. Looking more into detail and comparing 2021-2020, we see an 11% increase of venture fundraising to 7.5 billion euro. Buyout fundraising reached 36.3 billion, while growth funds show an increase of no less than 21% to 5.7 billion euro.

The first half of 2021, a record breaking 57.3 billion euro was invested into European companies. This is an increase of 38% compared to 2020 to a level of investment that has never been seen before. Especially venture capital investments (+85%, 10.2 billion) and growth investments (+280%, 17.5 billion) boost those impressive figures.

It is crystal clear that PE used a considerable part of the money the ECB has been printing and funneled it to companies. (Truth be said, significant amounts also go to governments, investments in the public domain, consumers … )

Important to note: although we focus now on PE in Europe, we see the same trends in the United States and western economies in general.

Fact #3: bank loans have become cheap.

Banks are eager to grant loans at historically low interest rates. Money is cheap. Moreover, companies and banks with cash surpluses are being penalized today by negative interest rates. As a result the value of those cash surpluses is not anywhere near the return expected by the shareholders. Putting that money to work, now more than ever, is the message.

Result #1: a sharp increase in M&A activities.

Global M&A deal value is skyrocketing. With more than 1 trillion USD M&A deal value, the first three quarters of 2021 already surpassed the total deal value of 2020. There’s no doubt the investment activity will surpass both 2018 and 2019 all over the world.

The effects are noticeable in a significant increase in the number of deals as well as in the average transaction value. In Europe, the year to year increase in total deal value is 36%. The United States and Canada see a 40% increase – 40% also being the global total rise in deal value.

If we look at the M&A activity numbers by industry, we see an interesting shift. Is it the availability of ‘free money’? Is it due to corona? Or is it a mix of both? In any case it is clear that we witness some major moves. Real estate/development is the number one industry in 2021 in terms of M&A investments, whereas in 2020 it only was number four. Financials and Industrials are respectively number two and three (coming from three and five). Information technology and healthcare fall back from a number one and two position in 2020 to four and five in 2021.

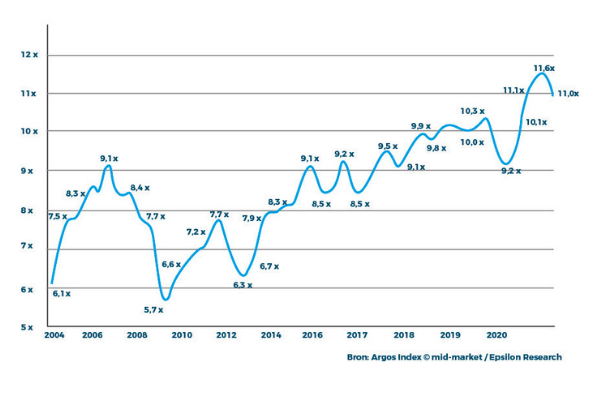

Result #2: impact on price.

The graph outlining the purchase prices of non-listed European SME’s shows the effects of the money the ECB pumped into the markets since 2008. In 2015 the average transaction value was again on its pre-financial crisis level, after which it continued to rise. Year after year more is paid for acquisitions – with the exception of ‘corona year’ 2020.

Looking forward: the risk of disruptions

The lay of the land is clear. But what about the (near) future? What are the risks that could affect, or even profoundly distort, the M&A market?

It is well known by now that the majority of businesses proved to be quite resilient during the covid pandemic. That is generally speaking of course, because there were also industries that thrived (healthcare and IT, for instance) and others that suffered (travel, retail, event sector).

However, there are risks emerging. The pandemic confronted us with a clearly overstretched – and thus failing – global supply chain, which resulted in a new geopolitical reality. Some even call it a cold war revisited with power blocks such as the US, Europe, Russia and China. Closer to home is the looming withdrawal of government support, which could lead to an increase in insolvencies and restructurings. The upside being M&A opportunities.

It still has to be confirmed if we are now confronted with a short term inflation hiccup or with a long term phenomenon. Inflation impacts the financing cost of companies and has a negative effect on their valuation. Growth firms, which are valued based on their expected future profits, suffer more from inflation in comparison to value companies. Companies which are penalized up until now for their cash surpluses, could have an advantage because they are not dependent on short term loans.

In our opinion, it is wise to be prudent in regard to the level of leverage used when engineering your acquisition finance, in order not to become too vulnerable to potential interest rates rising combined with margin erosion as a result of cost inflation. At the same time, the window of opportunity is still open to further develop your footprint in markets and industries you aim for. For sellers, the momentum is equally attractive although one needs to have a clear view on alternative investment opportunities for cash received when selling your company.

Contact one of our experts