Belgium has a specific tax regime for inpatriate workers and researchers aimed at strengthening the country’s attractiveness for international talent. This regime is subject to significant and retroactive changes applicable as of January 1, 2025.

The special tax regime: basic principles

Workers recruited directly abroad by a Belgian company, transferred or seconded to Belgium by a foreign company, may benefit from a favourable tax regime:

- In addition to the gross remuneration, the employer may grant employer costs of up to 30% of the annual gross remuneration, with an absolute cap of EUR 90,000 per year (original regime).

- Certain private costs may also be covered by the employer without constituting a taxable benefit in kind, including:

- moving expenses;

- temporary housing (up to 3 months);

- costs related to setting up the Belgian home during the first 6 months (ceiling of EUR 1,500);

- school fees at an international school in Belgium for nursery, primary and secondary education, provided the children are subject to compulsory education.

All of these expenses are exempt from personal income tax for the employee and exempt from social security contributions for both the employer and the employee. These costs can also be combined with other costs proper to the employer, such as teleworking allowances or internet allowances.

Strict conditions provided by the original legislation

When the regime was introduced in 2022, strict conditions were established:

- The individual could not have resided within a distance of less than 150 km from the Belgian border during the 60 months preceding the start of employment in Belgium.

- During that period, the individual could not have been subject to Belgian personal income tax or non-resident income tax on professional income.

- The annual taxable gross remuneration of the employee related to the Belgian employment must exceed EUR 75,000 per calendar year (excluding the tax-free portion of the special tax regime).

- When the individual is a researcher, the salary threshold does not apply when the employee:

- holds the required degree or has at least 10 years of relevant professional experience, and

- devotes at least 80% of the professional activity to R&D.

- The application of the special tax regime must be explicitly mentioned in the employment contract.

- The regime must be requested by both the employer and the employee.

The nationality of the employee is irrelevant (the regime may therefore apply to Belgian nationals).

The regime is also accessible to company directors.

Deadlines and duration of the regime

The application must be submitted to the Belgian tax administration within 3 months following the start of the activity in Belgium.

The regime is granted for a period of 5 years starting from the beginning of the employment in Belgium. An extension of 3 years may be requested within 3 months following the expiry date of the initial period.

In case of a change of employer, the regime may be maintained provided that a request for extension is submitted within 3 months following the start of employment with the new employer.

Relaxation of conditions and increase of the benefit (retroactive as of January 1, 2025)

In order to strengthen Belgium’s attractiveness for inpatriate executives and researchers, retroactive changes were adopted at the end of 2025. The following changes apply retroactively as of January 1, 2025:

- The tax-free portion of the remuneration may now reach 35% of the annual gross remuneration (instead of 30%).

- The absolute cap of EUR 90,000 per year is removed.

- The minimum annual gross remuneration (for non-researchers) is reduced from EUR 75,000 to EUR 70,000.

Uncertainty regarding the position of the Belgian social security administration

At this stage, the changes have only been incorporated into tax legislation, which creates uncertainty regarding the position of the Belgian social security administration.

If they do not align with the tax legislation, there could be:

- a 30% portion exempt from income taxes and social security;

- an additional 5% portion exempt from tax, but subject to social security contributions.

This situation would complicate payroll management. Moore has therefore sent an official letter to the Belgian social security administration requesting alignment with the tax legislation.

Practical examples

The calculations were made for a single taxpayer without dependants and based on the tax rates applicable for income year 2026.

Employer social security contributions were estimated at 27%.

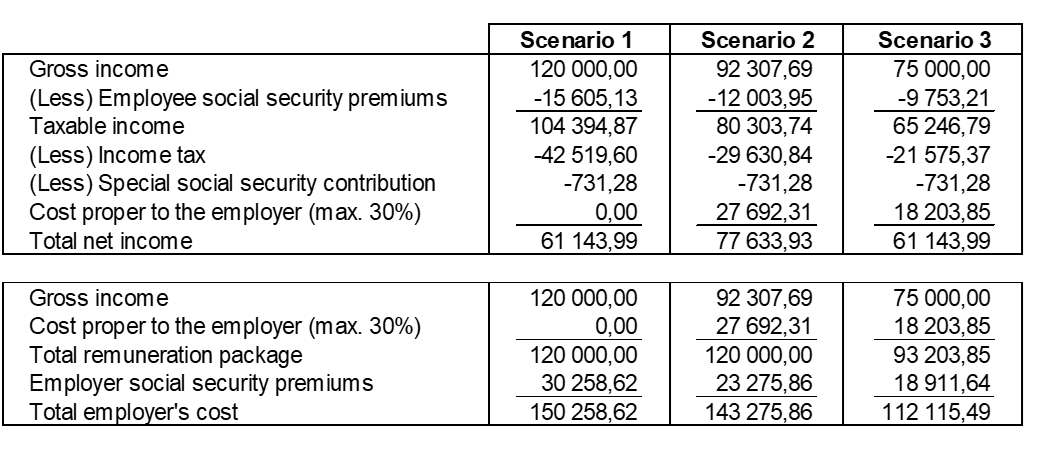

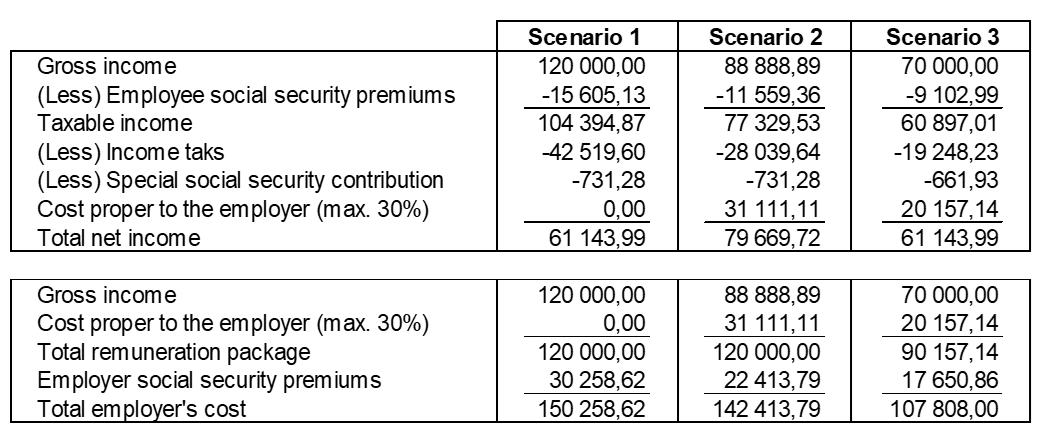

- Scenario 1: without application of the special tax regime. Total salary package of €120,000.

- Scenario 2: with application of the special tax regime (non-researcher) – same salary package as in scenario 1.

- Scenario 3: with application of the special tax regime (non-researcher) – same net salary as in scenario 1.

Original legislation (30%)

Amended legislation (35%)

We assume here that, in the long term, the Belgian social security administration will follow the tax legislation. The increased percentage of the tax-free portion (from 30% to 35%) has therefore also been exempted from social security contributions.

Action points following the changes

Employees who started employment before 01/01/2025

The reform opens a real optimisation window for employers who already have employees benefiting from the inpatriate tax regime.

It is now possible to significantly increase the portion of exempt allowances, provided that the following actions are taken:

- a review of the salary package, and

- a formal amendment of the employment contract.

This optimisation can be implemented not only for the future (from 2026 onwards), but also with retroactive effect from 1 January 2025, which makes it possible to quickly generate a net gain for the employee or substantial savings for the employer.

Employees who started employment in 2025 without meeting the initial criteria

A particularly favourable transitional regime targets employees hired in 2025 who did not initially reach the required minimum salary.

Where the annual gross remuneration is between EUR 70,000 and EUR 75,000, an application remains possible within a specific timeframe, offering a second opportunity to access the regime. As the law was published on 30 December 2025, the deadline is set at the 9th of April 2026. A contractual amendment is essential in order to secure the application of the regime.