Federal target group reductions – first employees

Since 1 January 2016 new employers have, for the engagement of their first employee between 1 January 2016 and 31 December 2020, received an indefinite exemption from social security contributions. For the next five employees there are target group reductions that are time-bound. As of 1 January 2017 the sums of the target group reductions for recruiting the third to the sixth employees have been raised, and have thereby also been awarded for an extended period.

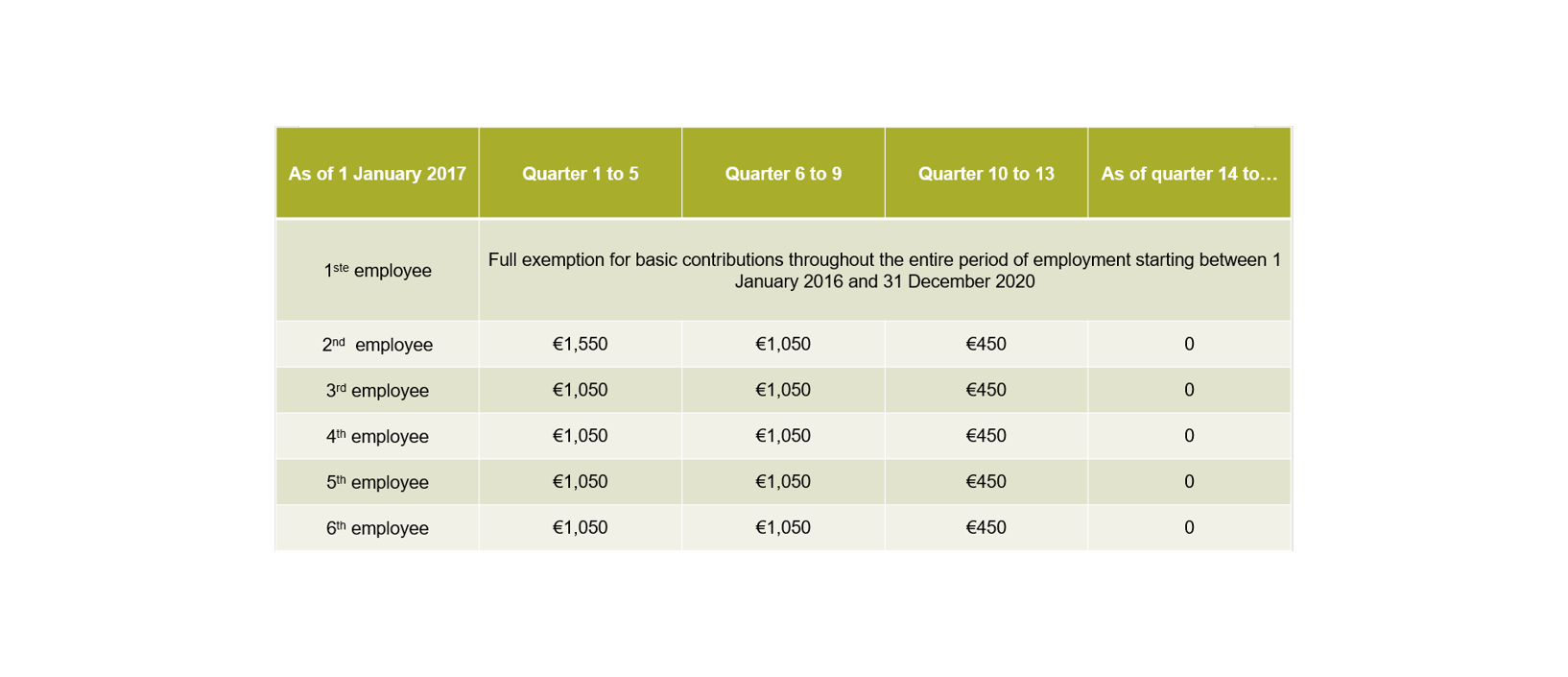

Lifelong exemption for the first employee

This must be the first person a new employer recruits. In order to be eligible for exemption for the initial employee, the employer must:

- Either never have had staff before, and so never have been required to pay social security contributions for employees;

- Or not have been subject to National Social Security Office (Rijksdienst voor Sociale Zekerheid – RSZ) legislation during the four quarters preceding the quarter in which the first employee is recruited.

If either of these conditions is met the RSZ shall check whether the employer does not, together with another employer, constitute a ‘technical business unit’ (technische bedrijfseenheid). This is because the exemption for the first employee must always pertain to a true additional recruitment for the technical business unit, and shall never be awarded for replacing an employee within the same technical business unit.

Full exemption for the employer’s basic social security contributions for the first employee is applicable for an indefinite period.

- The basic contributions are exempted in full, while certain special contributions remain payable (such as quarterly contributions to the annual leave, annual contribution to the annual leave, special contributions for workplace accidents, etc). These special contributions are dependent on the contract (white-collar/blue-collar), the size and the nature of the company (whether or not its objectives are commercial or industrial in nature) and the industry in which it operates.

- The first employee exemption is not personalised – recruiting the very first employee entitles the employer to the exemption. So each quarter the employer must state the employee for which he or she is exempted, as it is quite possible that the employee that first entitled the employer to the exemption is no longer employed. In practice the employer’s social security agency examines the ways in which the exemption can be optimised each quarter.

Extending the target group reduction for initial employeesThe introduction of the exemption for a first employee has also seen the existing target group reductions extended from five to six employees. In real terms this means that the fixed sums and the number of quarters to which the existing target group reduction was applied for the first through fifth employees before 1 January 2016 is passed on integrally to the second through sixth employees. As of 1 January 2017 the sums of the reductions have been raised and awarded for an extended period.

This new regulation is effective as of 1 January 2017. The employer who benefited from a reduced contribution in respect of the target group reduction before that date can continue to apply the old regulation (as was in force on 31 December 2016).

Contribution to the social security agency expenses

A new employer who registers with an accredited social security agency is also entitled to a contribution of €36.45 per quarter during those quarters in which he or she applies for a target group reduction for a first employee. For each quarter that the employer benefits for an initial employment, this contribution can also be received.

Regional target group reductions – Personal target group reductions

Flanders has opted to create new target group reductions for employing young people (under the age of 25), older people (over 55) and people with an occupational impairment (recipients of the Flemish support subsidy, or Vlaamse Ondersteuningspremie). The introduction of these new target group reductions is coupled with a drastic simplification, which has seen a number of existing measures scrapped since 1 January 2016 or 1 January 2017, including the Activa, Activa Start, Activa Handicap, the 50+ employment bonus and the target group reduction for restructuring measures. The replacement transitional measure involves phasing out, with the awarded benefits in place on the date upon which the measures were scrapped continuing until 31 December 2018 at the latest.

Target group reduction for young employees

This new target group reduction replaces the target group reduction for extremely unskilled, unskilled and semiskilled youth and for those under the age of 19. In practical terms the new target group reductions consists of two separate reductions:

The target group reduction for young employees – semiskilled and unskilled:

- Unskilled youngsters are ones who have not been awarded a secondary education diploma or certificate certifying their completion of the 2nd year of their third two-year cycle of education. The Flemish Employment and Training Service (VDAB) certifies and determines who is eligible, and it informs the RSZ electronically of the level of education attained;

- Semiskilled youngsters have not exceeded a secondary education diploma or certificate certifying their completion of the 2nd year of their third two-year cycle of education. The VDAB certifies and determines who is eligible, and it informs the RSZ electronically of the level of education attained.

The target group reductions for young employees – apprentices who are alternating between studying and working (alternerend leren) and those following part-time vocational secondary education (DBSO or deeltijds beroepssecundair onderwijs) and who have a part-time employment contract:

- Apprentices who are alternating between studying and working as referred to in article 1bis of the Royal Decree of 28 November 1969;

- Youngsters following part-time vocational secondary education who, as part of completing specific alternate courses, are employed under a part-time employment contract.

So how much reduction can one expect?

- The target group reduction for employment while studying amounts to €1,000 per quarter for the 1st to the 7th quarters for the duration of that person’s employment. Once the student has graduated, the employer can still apply for the young unskilled and semiskilled employees’ reduction, where the quarters in which this reduction was applied do not count for the unskilled and semiskilled employees’ reduction.

- The target group reduction for the employment of unskilled young employees (under the age of 25) amounts to €1,150 per quarter for quarters 1 through 7.

- The target group reduction for the employment of semiskilled young employees (under the age of 25) amounts to €1,000 per quarter for quarters 1 through 7.

What are the conditions for benefiting from these target group reductions?

- Youngsters up to the age of 25 working at or dependent on an operational unit in Flanders who were employed after 1 July 2016.

- The quarterly salary reference wage for the young employee is less than the determined salary threshold:

- €7,500 during the quarter in which the person was employed and in the three following quarters;

- €8,100 during the following four quarters.

- The unskilled and semiskilled youth, as well as those following part-time vocational secondary education must create an electronic file (called ‘portfolio’) with the VDAB.

Target group reduction for elderly employees

This new target group reduction replaces the existing target group reduction for the elderly. The sum of the target group reduction depends on the age of the employee (over 55) and whether the employee is newly employed or whether it is a case of continued employment.

Target group reduction for employing elderly non-working jobseekers:

- A fixed reduction of €1,150 for quarters 1 through 7 if the recruited person is at least 55 and is not yet 60 on the last day of the quarter in which he or she was employed;

- A fixed reduction of €1,500 for quarters 1 through 7 if the recruited person is at least 60 and has not yet reached retirement age on the last day of the quarter in which he or she was employed.

Target group reduction for existing elderly employees:

- A fixed reduction of €600 if the existing elderly employee is at least 55 on the last day of the quarter;

- A fixed reduction of €1,150 if the existing elderly employee is at least 60 on the last day of the quarter.

What are the conditions for benefiting from these target group reductions?

- The reduction is only applicable as of 1 July 2017 and is limited to private sector employees.

- Elderly non-working jobseekers employees cannot have been working for the same employer in the four quarters preceding this employment and must register with the VDAB as non-working jobseekers.

- The reference quarterly salary for the elderly employee for the current quarter must be less than €13,400.

The Flemish support subsidy

The extant Flemish support subsidy (Vlaamse ondersteuningspremie – VOP) remains in place, but is extended to include employees in the social economy and self-employed persons with a sideline activity. The intention of the VOP is, on the one hand, to compensate employers for the loss of earnings for an employee with an occupational disability, and on the other to stimulate the integration of that employee in the job market. The subsidy is a percentage of the capped reference salary and is, under normal circumstances, awarded over 20 quarters as of the quarter in which the application was submitted, with such according to the following schedule:

- Quarter 1-5: 40%

- Quarter 6-9: 30%

- Quarter 10-20: 20%

The reference salary is equal to the gross salary plus the standard employer’s social security contribution and less the social security reduction. In the event of fulltime employment, the reference salary is also capped at twice the guaranteed average minimum monthly income.

Employment incentive for long-term jobseekers

The new Flemish employment incentive for long-term jobseekers was introduced under the Royal Decree of 17 February 2017 and has been in effect since 1 March 2017. This employment incentive replaces the job benefit and the target group reduction that was previously known as the ‘Activa plan’. The employment incentive will be awarded by the VDAB to companies that comply with a number of conditions:

- Employing a non-working jobseeker who, at the time of being employed, has been registered as a non-working jobseeker for at least two years and who is over 25 and not older than 54;

- An employment contract for an indefinite period is signed;

- The employee is employed in an operation in the Flemish region.

The employment incentive is paid out in two parts:

- Max. €1,250 in the event of continuing employment for 3 months;

- Max. €3,000 in the event of continuing employment for 12 months.

In the event of part-time employment, the incentive is awarded on a pro rata basis. The company must submit its application within three months of employment commencing. For any persons employed between 1 January 2017 and 1 March 2017 the application must be submitted before 1 June 2017.3.

Conclusion

The introduction of the new target group reductions as a result of the 6th state reformation has resulted in a considerable simplification of the existing target group reduction system. The restructuring means that the Activa, ActivaStart, Activa Handicap, the 50+ employment bonus and the target group reduction for restructuring have all been scrapped, although the benefits awarded under those systems that are ongoing at the time of their scrapping will continue until 31 December 2018 at the latest.