It concerns a target group reduction in the event of a collective reduction in working hours, additional Coronavirus related time credit and end-of-career time credit from the age of 55.

It is important that this recognition was/is granted at the earliest on 1 March 2020 and at the latest on 31 December 2020. In other words, it relates to companies that generated negative results over the past two financial years, companies that are introducing collective redundancies and companies that suffered at least 20% unemployment last year.

The recognition procedure differs depending on the reason invoked by the employer. It is the same as that previously applied during non-Covid times, but in this case recognition can be obtained under these measures without the need to conclude a collective labour agreement introducing the system of unemployment with company allowance (SWT). It should also be noted that it takes approximately two months for recognition to be granted.

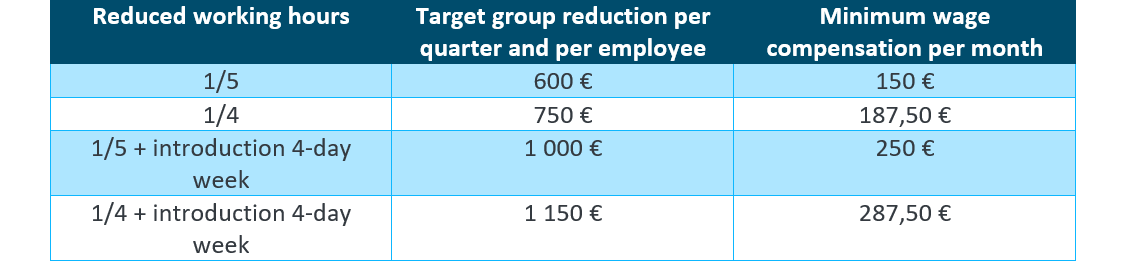

Collective reduction in working hours

Employers, who cut working hours by 1/5th or 1/4th, shall benefit from a target group reduction in national insurance contributions for each employee and each quarter. If the reduction in working hours coincides with the introduction of a 4-day week, the amount of the reduction in social security contributions will be increased.

The temporary adjustment in working hours and temporary introduction of a 4-day week can only be introduced for a maximum period of one year. The start and end dates of the period of reduction in working hours must be within the period of recognition as a company undergoing restructuring or in difficulty.

Employees whose working hours are reduced and consequently receive lower wages shall receive compensation at the expense of the employer. This compensation shall amount to at least three-quarters of the amount of the lump-sum reduction in social security contributions.

Coronavirus related time credit

The Coronavirus related time credit provides the option to reduce work activities by 1/5th or to a half-time job for a maximum period of 6 months, without this period of Coronavirus related time credit being added to the maximum duration of the regular time credit. Contrary to the regular time credit scheme (CAO 103), employees are not obliged to provide substantiation.

Coronavirus related time credit shall be applied for a minimum of one month and a maximum of six months. Coronavirus related time credit can be extended, whereby the new period does not have to immediately follow the previous one. However, each individual period must be at least one month and the total duration shall not exceed six months.

The overall duration of the Coronavirus related time credit must fall within the period of recognition as a company in difficulty or undergoing restructuring.

Employees who reduce their working hours under the Coronavirus related time credit scheme shall be entitled to an interruption allowance from the National Employment Office. The amount of this benefit shall be the same as that for ordinary time credit.

Coronavirus related end-of-career time credit

Collective Labour Agreement No 103 stipulates that an employee is only entitled to a half-time or 4/5th end-of-career time credit with benefits from the age of 60. This age limit is reduced to 55 under the current crisis measures.

In order to qualify for the end-of-career time credit with benefits, the employee must be able to corroborate a professional history of at least 25 years. Contrary to the normal end-of-career time credit, the Coronavirus related end-of-career time credit can be taken for a minimum period of 1 month instead of the minimum period of 3 months for a half-time end-of-career time credit and 6 months for a 4/5th end-of-career time credit. The end-of-career time credit can be taken until retirement age.

Contact one of our experts

Saskia Lombaerts

Partner Tax & Legal Services

Contact us