What is involved?

Costs reimbursed by an employer are costs that an employee or director incurs on behalf of the company. As far as the employer or company is concerned these are business costs.

The reimbursement of these costs is exempt from social security contributions and withholding taxes for the beneficiary employee or director. Except for a few exceptions and depending on the actual costs, they are tax deductible for the employer.

An employer may allocate fixed expense allowances subject to certain conditions. It is also possible to reimburse the actual costs as a variable cost allowance based on supporting documentation.

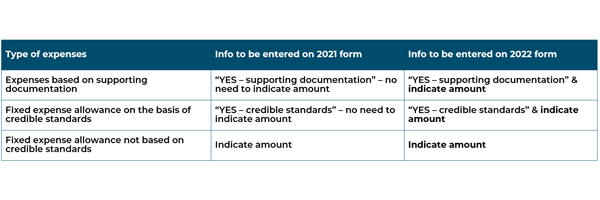

On the 281.10 and 281.20 tax return forms these costs can still be processed fairly easily for the 2021 income year.

Changes from income for 2022 onwards

A circular letter dated 26 February 2021 concerning employers' contributions for working from home highlights a change in the form requirements for expense reimbursements as of 1 January 2022. Although much is still uncertain, we would like to clarify what we already know.

Since 1 January 2022 the obligation to provide information has been tightened. In particular for variable allowances granted to an employee or director to reimburse actual costs incurred on behalf of the employer. Henceforth, you must account for these costs on the individual forms and include their actual value, which entails considerably more administrative work.

Overview of entries on 281.10 and 281.20 forms

Who paid for the expenses?

When receiving an invoice or receipt, you need to check who paid it.

- The employee has advanced the expenses

If the expenses are not directly invoiced in the name of the company or employer concerned and the employer then reimburses them, they must now be included on sheet 281.10. The payment must be traceable when the amount is paid in cash or transferred to the employee’s personal account. Some accounting systems provide the option to indicate this when entering invoices. If this is not possible, you need to keep separate records.

- The director has advanced the expenses

The same applies to directors. If business expenses are advanced privately, they must be included on the 281.20 form. Reimbursements transferred to a current account or paid in another way must be allocated. If you pay business costs privately and book them to the current account, they must be included on the form.

Penalty for incorrect entries

Failure to keep these records correctly will result in sanctions.

Expenses that are reimbursed on the basis of supporting documentation but that are incorrectly entered will still be deductible within the company but will result in an administrative penalty. It is as yet unclear whether the penalty will be applied per form or per infringement. The amount of this administrative penalty is also still unclear.

Contrary to what applies to fixed expense allowances, not entering the amount correctly does not lead to the application of the undisclosed commissions levy.

Which actual steps can you take?

In order to keep the administrative burden to a minimum and avoid potential fines where possible, it is advisable to:

- obtain as many invoices/receipts as possible in the name of the company or employer, even if they are paid personally by an individual. The company or employer will then reimburse the expenses without the need to enter them on the form.

- As little as possible should be written off via the current account. Costs should actually be refunded if a private payment was made without an invoice/receipt in the name of the company or employer. This way it is clear which costs must be entered on the form by using a single ‘employer reimbursed expenses’ account.

If you would like further information concerning this amended declaration duty, please do not hesitate to contact our experts.

Contact one of our experts