Taxable capital gain on property

When does a person achieve a taxable capital gain on property or land located in Belgium?

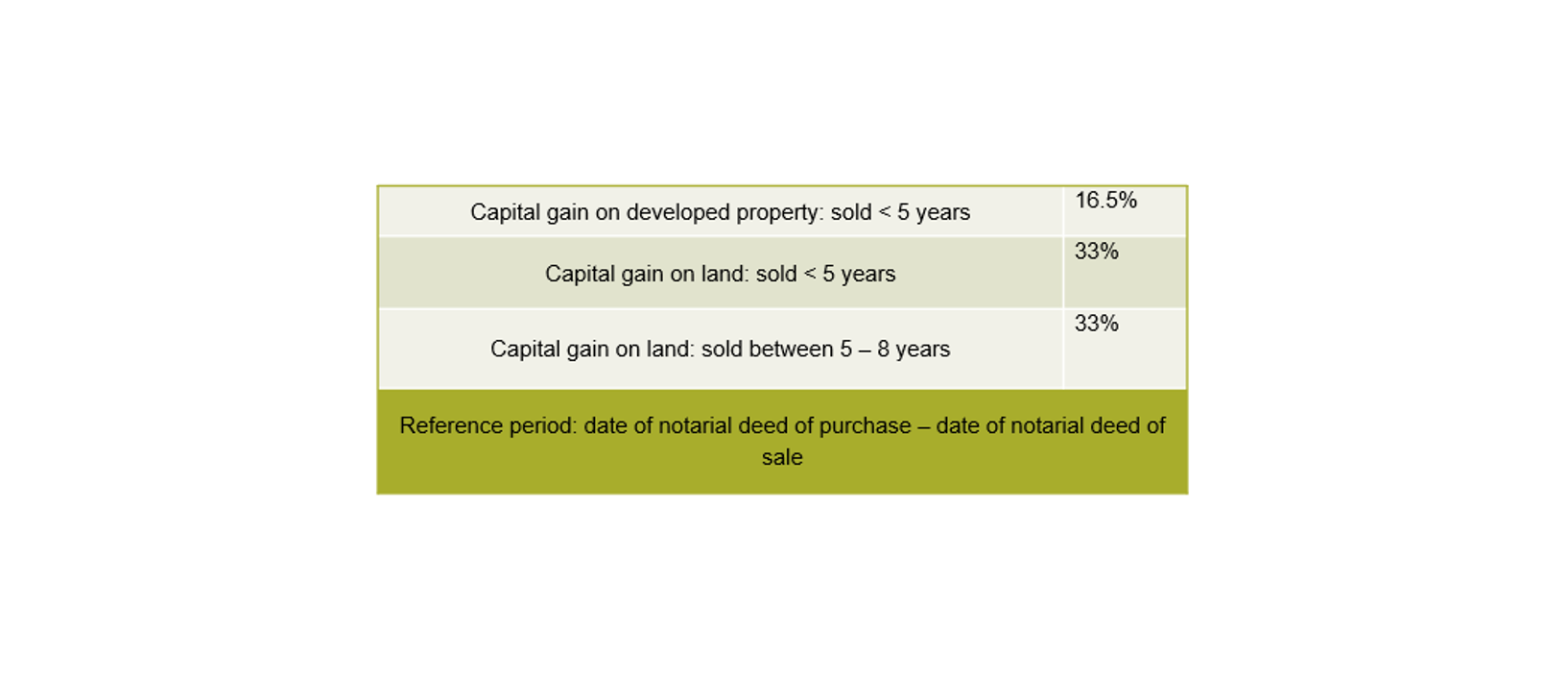

If you sell developed property within five years of purchasing it at a profit, then you will be taxed on that capital gain. The reference period for this is the dates of the notarial deeds of sale and purchase. This capital gain is taxed at a rate of 16.5%. But if you wait longer than five years before selling the property, the capital gain is not taxable.

You will also be taxed on the capital gain if you sell land at a profit, with the tax authorities taking two periods into account: if you sell the land within five years of purchasing it, the capital gain is taxed at a rate of 33%, a rate that is halved to 16.5% if you sell the land between five and eight years after purchasing it.

The capital gain on the sale of developed property and/or land that is obtained as a gift is taxable if the sale takes place within three years after the instrument of gift is executed and within five and/or eight years of its purchase by the giver.

If you have constructed a building on land that you obtained for valuable consideration or as a gift, you will also be taxed on the capital gain if:

- construction started within five years of obtaining the land for valuable consideration by the taxpayer or by the giver

- the developed land is sold within five years of the date of the first time the building was occupied or rented out.

A brief summary:

The above tax rates do not include municipal tax.

So what exactly gets taxed?

How is the capital gain actually calculated?

The capital gain is not solely the positive difference between the purchase price and the sales price, and there are a number of concepts that must be taken into account.

- The net sale value: this is the sale value less the costs incurred in accomplishing the sale, primarily estate agent fees but also expenses such as advertising. Should the sale value be less than the sum upon which VAT or the registration duties were levied for the sale, then the latter higher value is taken to be the sale value.

- The fixed purchase value: the fixed purchase value is the purchase value plus 25% fixed purchase costs or the actual purchase costs if they exceed 25%. For every year between the purchase and sale, this value is raised by 5%. If you purchased property and had a professional constructor refurbish it, then those expenses can be added to the purchase value. Should you have received any compensation due to damage to the sold building, then that compensation will be deducted from the purchase value.

The positive difference between the net sale value and the fixed purchase value is the capital gain that will be subject to taxation. This calculation must be substantiated in your personal income tax return using a specific annexe.

Exclusions from the capital gains tax

In a number of cases capital gains tax is not payable:

- Your own residence

If you sell the residence that is your principal place of residence and that houses your family within five years at a profit, capital gains tax is not payable. You must however have occupied the residence for at least six months in the 12 months preceding the sale.

- The sale of inherited property

The capital gain on the sale of developed property or land within five or eight years that was inherited is not subject to taxation. Please note that if the tax authorities decide that the value of the property as listed in the inheritance tax declaration was too low, they can dispute this value for up to two years after the declaration is submitted.

- Expropriated property

- Property owned by minors, persons under provisional administration and persons without legal capacity.

Conclusion

In brief, we wish to emphasise that you must seek out all information in advance before engaging in property transactions involving property recently purchased or received. In a great many cases a considerable amount of capital gains tax can be avoided if you plan properly. So always seek the advice of an expert.

Our team is always available to answer any questions you may have in this respect.